Are you an early-stage startup founder, with zero sales or just the first few sales? Or launching a new product? Or entering a new market?

And are you wondering how to achieve product-market fit, in order to get ready for growth?

If the answer is “yes”, then you’re in the right place. In this article, I give you turn-by-turn directions on how to achieve and prove product-market fit.

Product-market fit has always been a mysterious thing.

As a founding team member of 13 startups, mostly in B2B SaaS, I’ve been through the cycle of zero-to-product-market fit quite a few times by now, while growing some of them to over 200 employees.

During this period, whenever I asked my mentors, investors, or VCs to explain product-market fit in tangible terms, they’d always reply along the lines of: “It’s really hard to define – you’ll know it when you see it.”

If I described the situation of my startup and asked whether I had reached product-market fit, the answer was usually: “If you have to ask, you probably haven’t.”

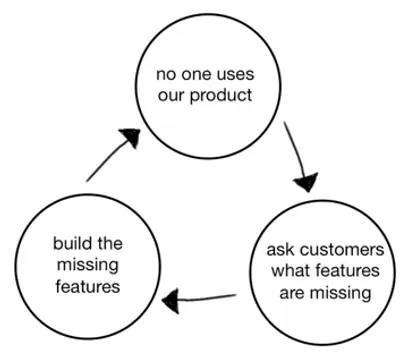

As for how to reach product-market fit, the most common advice I got was to just ask my customers and build what they want.

But that doesn’t always work, does it?

More or better products don’t always mean greater growth. We can all name at least a few examples of not-so-great products that made big companies – and vice-versa. David Bland, one of the gurus in San Francisco for product-market fit, calls it the product death cycle – aka death by feature.

Other definitions of achieving a product-market fit that doesn’t really work either:

When you have more customers than you can handle.

When you ask your customers how they’d feel if your product didn’t exist tomorrow, and the majority of them say “very unhappy”.

These are pretty vague (not to mention inaccurate) explanations.

At my core, I’m an engineer – and such approaches don’t really resonate with me. I see things in terms of processes and systems, which should be predictable and repeatable.

In this guide, I’ll provide a concrete, recognizable, measurable definition of product-market fit – based on my experience with 13 different startups. Then, I introduce an easy-to-understand framework that you can use to achieve product-market fit.

Not only that, but you’ll also be able to tangibly prove that your startup has achieved this goal and is ready to be in growth mode.

All kinds of startups will find value in this article, but it’s most relevant for B2B companies since my experience lies mainly in that area.

So first, we’ll get to a definition of measurable product-market fit. Then, we’ll go through the step-by-step process for you to achieve it.

Defining Product-Market fit

What is product-market fit? And how do you know when you’ve achieved it?

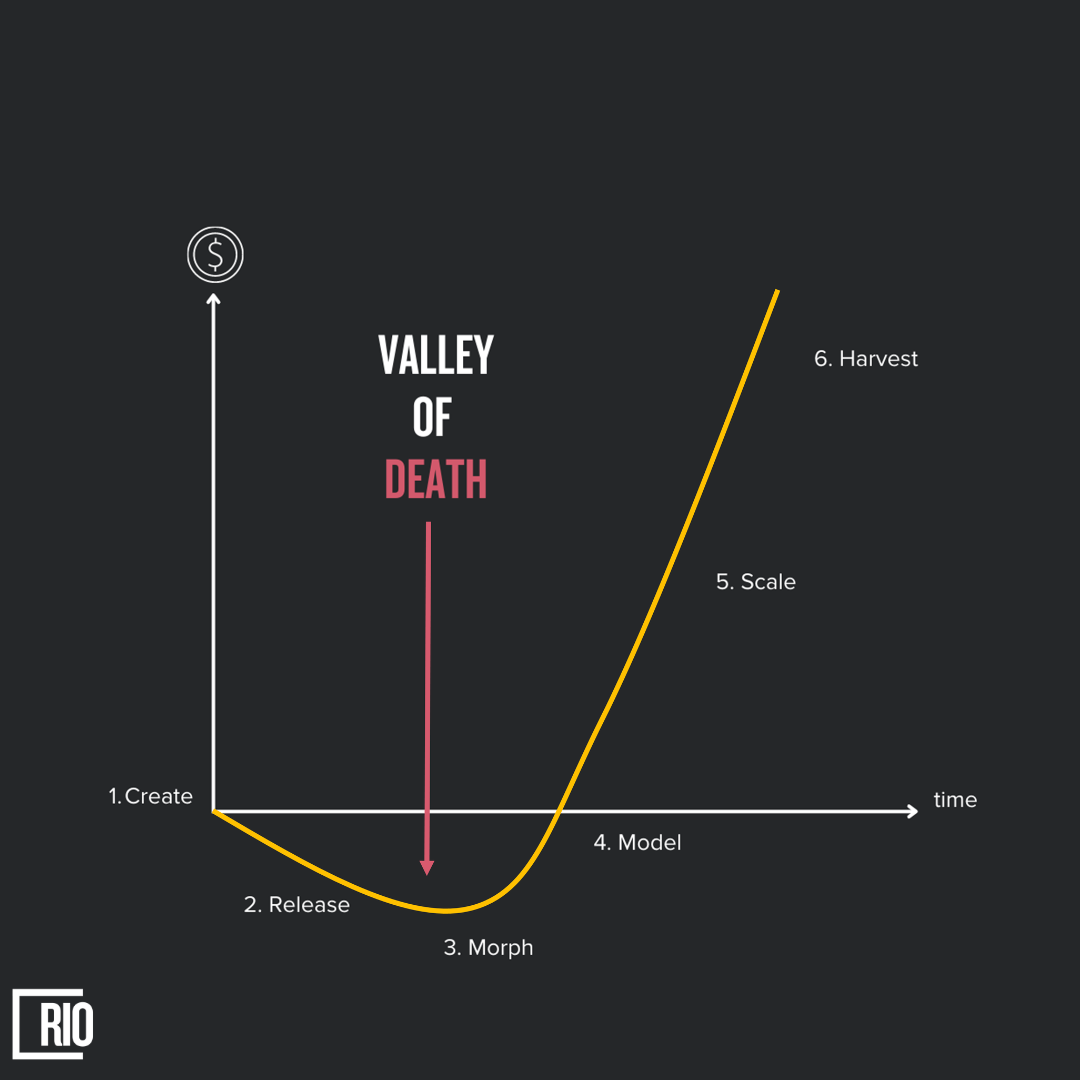

To start with, take a look at this “valley of death”. Where do you think product-market fit happens?

Product-market fit is around point 4 in this graph. When you achieve it, you’re ready to grow.

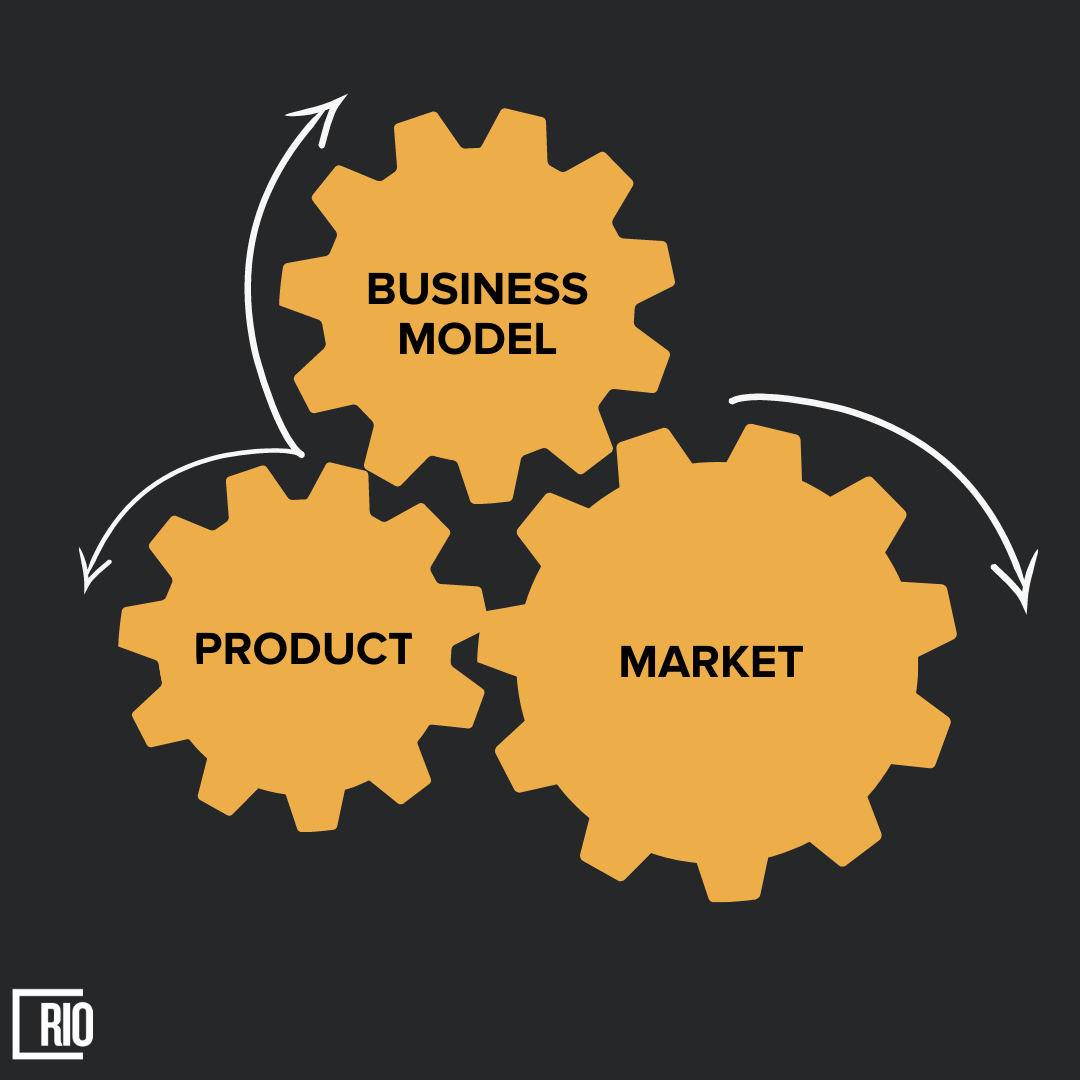

Basically, the real product-market fit is between the product, market, and business model. That means your product is a fit with the market you’re trying to serve, and at the same time, your business model resonates with your target customers.

Based on this understanding, we can say:

💡

Product-market fit is having [predictable sales] of [a product] with [positive Return on Investment (RoI)].

Let’s look at each variable in the sentence above:

Product is [a solution] that helps your [target customer] achieve [success] by solving [a problem] they have.

In the most fundamental sense, gross positive RoI = Average Annual Revenue Per User (AARPU) or Life Time Value (LTV) > Cost of Acquiring a Customer (CAC).

And predictable sales are achieved when you know that if today you reach out to [x target customers] with [a message], you’ll have [y sales] in [z days], with [a, b, and c steps] in your sales funnel.

P.S. – I will use AARPU instead of LTV for the rest of this article for simplicity.

P.P.S. – I am not including the Cost of Serving a customer in the RoI, also for simplicity. If you have a considerably high Cost of Serving your customers – one simple way is to use Gross Profit instead of AARPU.

That leads us to the full definition:

Product-market fit is knowing that if today you reach out to [x number] of [target customers] with [a message], you’ll have [y sales] in [z days] with [a, b, and c steps] in your sales funnel, for [a solution] that helps them achieve [success] by solving [a problem] they have while having your [AARPU] more than [CAC].

Once you have the values for all these variables, you’ll be able to know and prove that you have a product-market fit and that you’re ready to scale.

P.S. – Obviously, this is based on the assumption that your product works well and helps your customers achieve success.

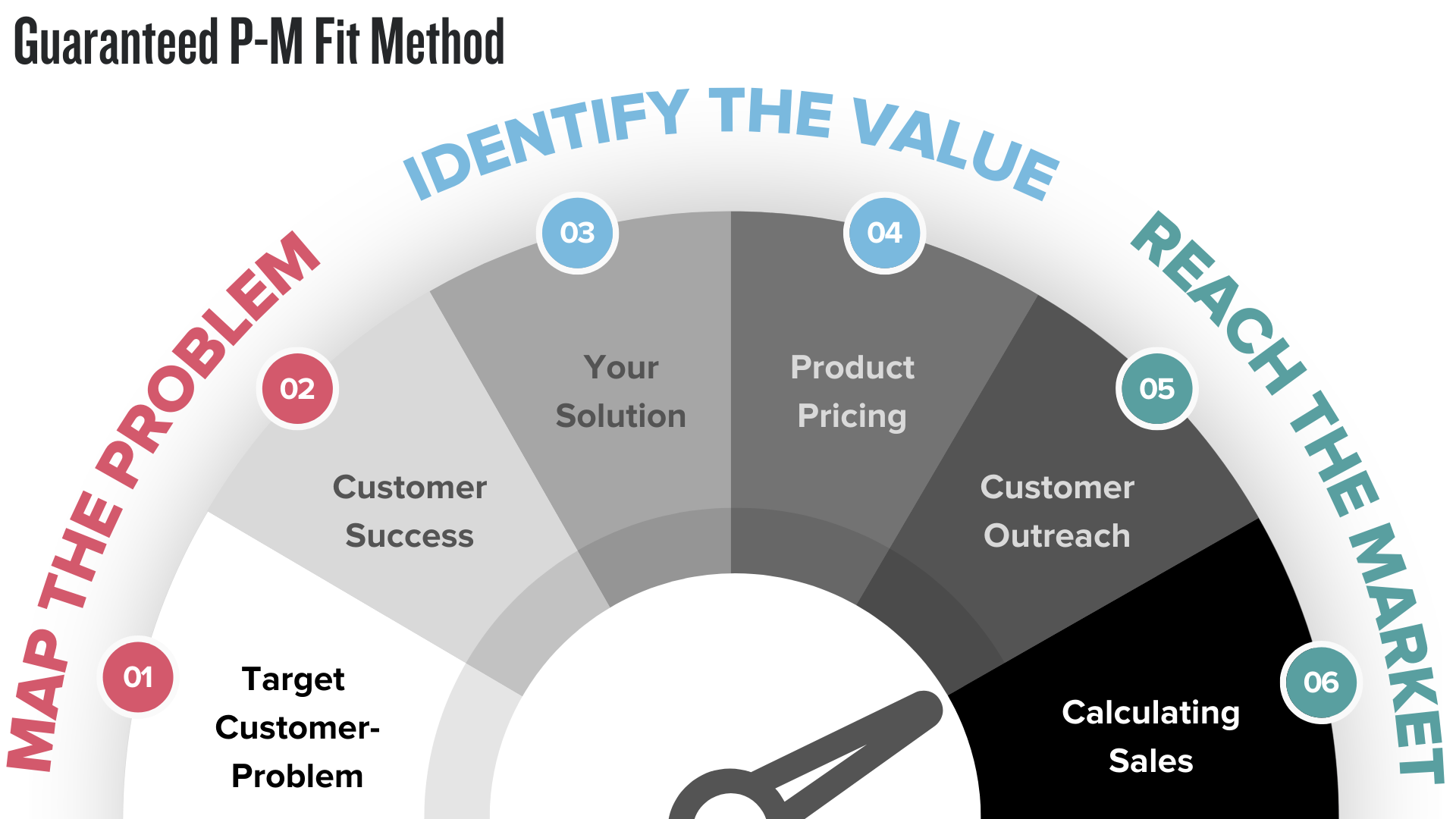

Guaranteed P-M Fit Method

Now, let’s see how you can find the values for these variables for your company, using my Guaranteed P-M fit method.

Let’s take a look at each of the 6 levels:

The target customer and problem are the fundamental building blocks of the entire structure. They’re closely connected together.

Then comes success. Think of it as a before-and-after scenario: problem = life before using your product, and success = life after using your product.

The solution is your product. Essentially, it’s how your customer goes from problem to success.

Then there’s pricing, based on how big the difference is in your before-and-after scenario, and what other solutions are out there.

Next up, is customer outreach. This is how you get your customer’s attention.

Calculating sales is the journey from your customer giving you attention to giving you money. Based on this, you know how much it’s going to cost you (CAC). With all the above information, you can easily calculate x, y, and z: how many people become your customers (y sales) out of the people you contacted (x customers) and how long it takes to complete the process (z days).

Just by looking at this framework, you can see that:

Whenever you change anything at one level, you’ll need to adjust and recheck everything above that level. For example, if you change the solution, you need to re-verify and redesign everything above it, starting with pricing.

Product-market fit is a spiral model, not a one-time exercise. As a company, you’ll never achieve it once and for all. You’ll always be improving your product, tweaking your messaging, expanding to another customer segment, and so on.

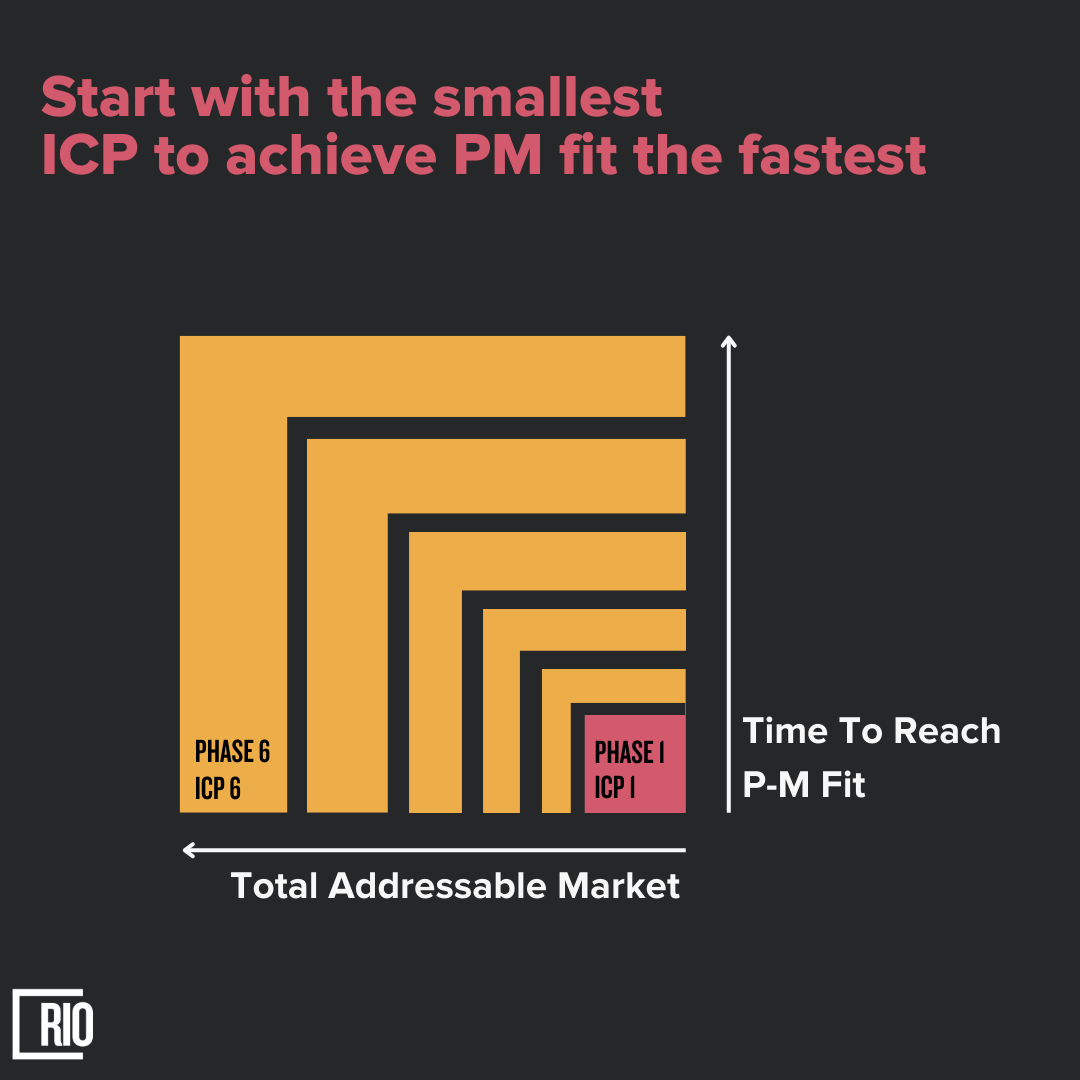

On the other hand, if you start really niche, you can reach product-market fit quite early. Then, you’ll always have it for a specific segment and a specific use case. And if you expand one step at a time – e.g. widen your target segment, increase the level of success your product provides, provide a better solution – then you’ll continue to reach quick product-market fit for each mini-expansion as shown in the image below.

Simply by changing the variables, you can speed up or slow down your time to Product Market Fit. Basically, the narrower the target segment you start with, the faster it’ll be to achieve product-market fit for doing just one thing that helps this particular niche.

If you look back at the histories of today’s successful companies, every major company started with a very small market. Amazon began with books that you couldn’t find in bookstores. Facebook focused on Ivy League schools. PayPal started with eBay users. Zenefits focused on Californian tech companies with 100-300 employees. Zappos took off with shoes. Airbnb began with one city – San Francisco, and Google indexing a single topic – Linux.

In a way, most successful companies have been in a state of continuous product-market fit from early on – while simultaneously discovering new avenues to expand and reach new product-market fit at each step.

Now that you know the definition and overall framework, I’m going to take you through the different steps to help you achieve product-market fit quickly and efficiently. This will put your startup on the path to growth, taking it out of the valley of death.

MAP THE PROBLEM

1. Target Customer - Problem

If you know what problem you want to solve but have no idea how you’re going to solve it, that’s fine – just write down the problem and who has it.

But if you’re like most of us, who simply have an idea – well, now you have work to do.

Step 1: Split your idea into problem and solution.

Are you unable to write down the problem you’re solving? Do you just have a solution idea right now? If yes, you’ve got to invest some serious time and effort into getting the fundamentals in place.

Right now, forget about the solution and just focus on the problem.

You need to think of the problem in its purest possible form. The risk here is that when you’re thinking about the problem, you might slip the solution into it.

When NASA was sending astronauts into space, they knew they wouldn’t be able to use ballpoint pens out there because of zero gravity. So, one of their subcontractors, Paul C. Fisher of Fisher Pen Company said: I think we can create a pen that writes in space.

This is a classic example of a solution polluting the problem space. Can you guess what the solution is?

It’s a pen. The pen is a solution. The pure problem would be: I think we can create something that astronauts can use to write in space.

It would be even better for you to ask: Why do astronauts need to write in space at all?

Let’s say the answer was: Astronauts need to take notes while working on xyz in space.

Then the problem statement would be: I think we can create something that helps astronauts take notes while working on XYZ in space.

This last statement is purely in the problem space, whereas the first statement was corrupted by a solution (I think we can create a pen that writes in space.).

After determining the problem, you need to split it into as many independent pieces as you can. If multiple customer segments face the same problem, list all the segments you can think of and see if there are some minor differences in the exact hypotheses of their problem.

You may even have multiple ideas or an idea/product that solves multiple problems. You’ll need to break this down further and write down each problem – as well as who has that problem.

Step 2: Choose a niche.

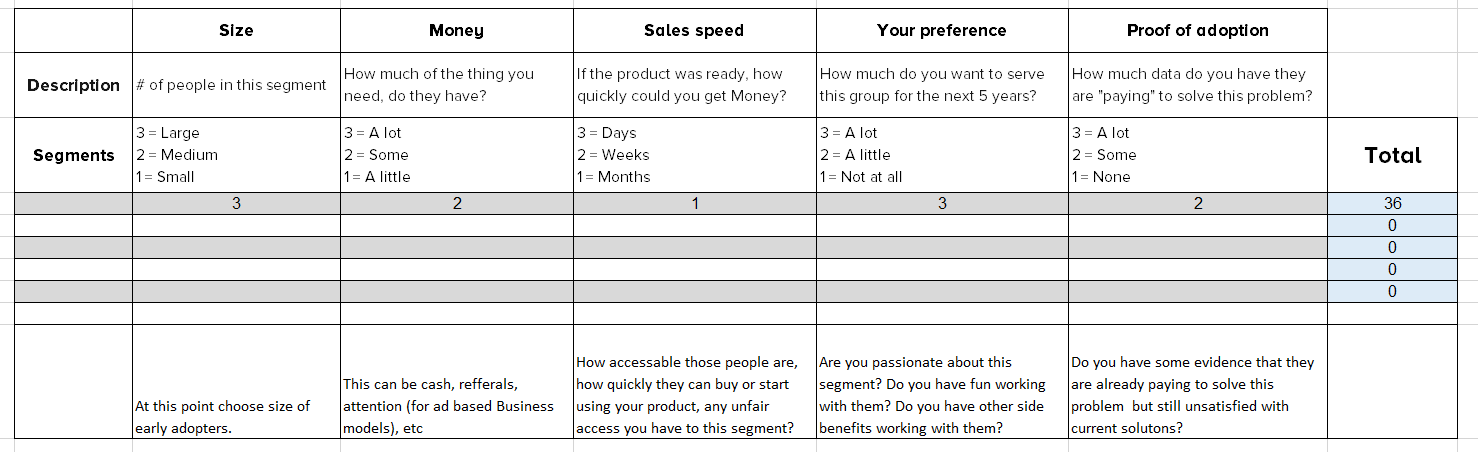

You might not have the resources to go after and test every segment and every detail of the problem you hypothesized, so you’ll need to prioritize.

At this stage, you can do a quick prioritization based on the knowledge and assumptions you already have. As a startup, you probably can’t do months of research to figure out which market you should even “test” first.

Chances are that whatever target customer you came up with in Step 1, you can further sub-segment them in more than one way.

Here’s an example to make the process clear.

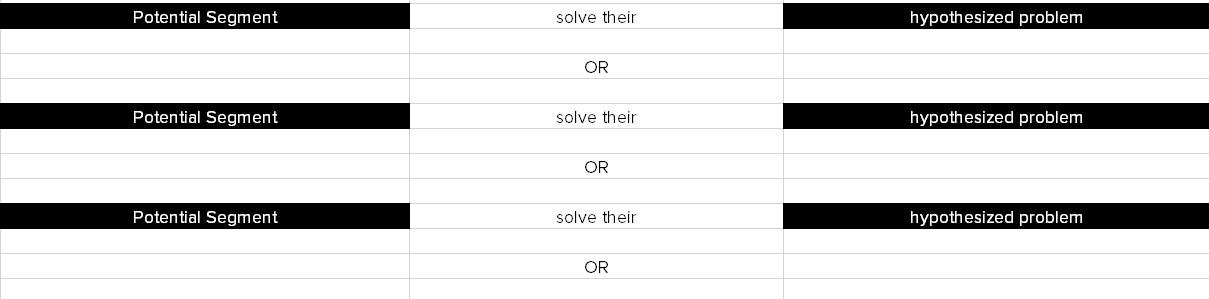

Let’s say this is the problem you want to focus on: independent professionals spend too much time every day filing bills and doing taxes. You can easily think of different professional segments that face this issue – doctors, lawyers, business consultants, etc.

Write down these segments in the table below, giving values to different parameters. Don’t worry about getting it exactly right – the values at this stage are simply based on what you already know or your gut feeling.

Then multiply the values in all columns in each row to get a total value. The highest number is your first priority segment.

Now take the segment with the highest priority and break it down further.

Say, doctors, emerge at the top in your segmentation. This can be narrowed down into smaller sub-segments.

For example, doctors who are fully independent, doctors who have a private clinic with 2-5 other doctors, doctors running super-small hospitals with a staff of 5-20 people – or even groups like psychiatrists who receive money directly from patients and might have different billing problems than surgeons who are independent but mainly work with on-demand calls from hospitals.

By this point, hopefully, you have one niche-enough target segment with which you can go ahead and test the problem hypothesis.

P.S. – The above are templates that have worked well for me in the past. Feel free to add and delete columns as suits your own unique case.

P.P.S. – It’s also possible to simply have all the columns in one template, list all the segments from lawyers to surgeons, and prioritize in a single step. But I’ve found that splitting the process into two (like above) helps you focus and dig out more niches.

Step 3: Validate your assumptions.

The problem you identify could be something you’ve personally faced. Maybe you even know a bunch of people just like you who have the same problem.

But if you’re like most founders, you probably have a problem and target market “hypothesis”. You think the problem exists, but you haven’t yet validated it. You might assume that the problem is so obvious that it doesn’t really need validation.

That would be a mistake.

In Paul Graham’s words, “by far the most common mistake startups make is to solve problems no one has.”

So, it’s crucial for you to make sure that your problem really exists. Even if you’ve faced it yourself, you’ve got to see how other people explain it to you and understand their experiences.

Pick the group that came out on top in your second segmentation above – you now need to check if your assumptions about them are correct. Do they really have the problem you think they have? Do they consider it a serious issue? Are they interested in solving it? And so on.

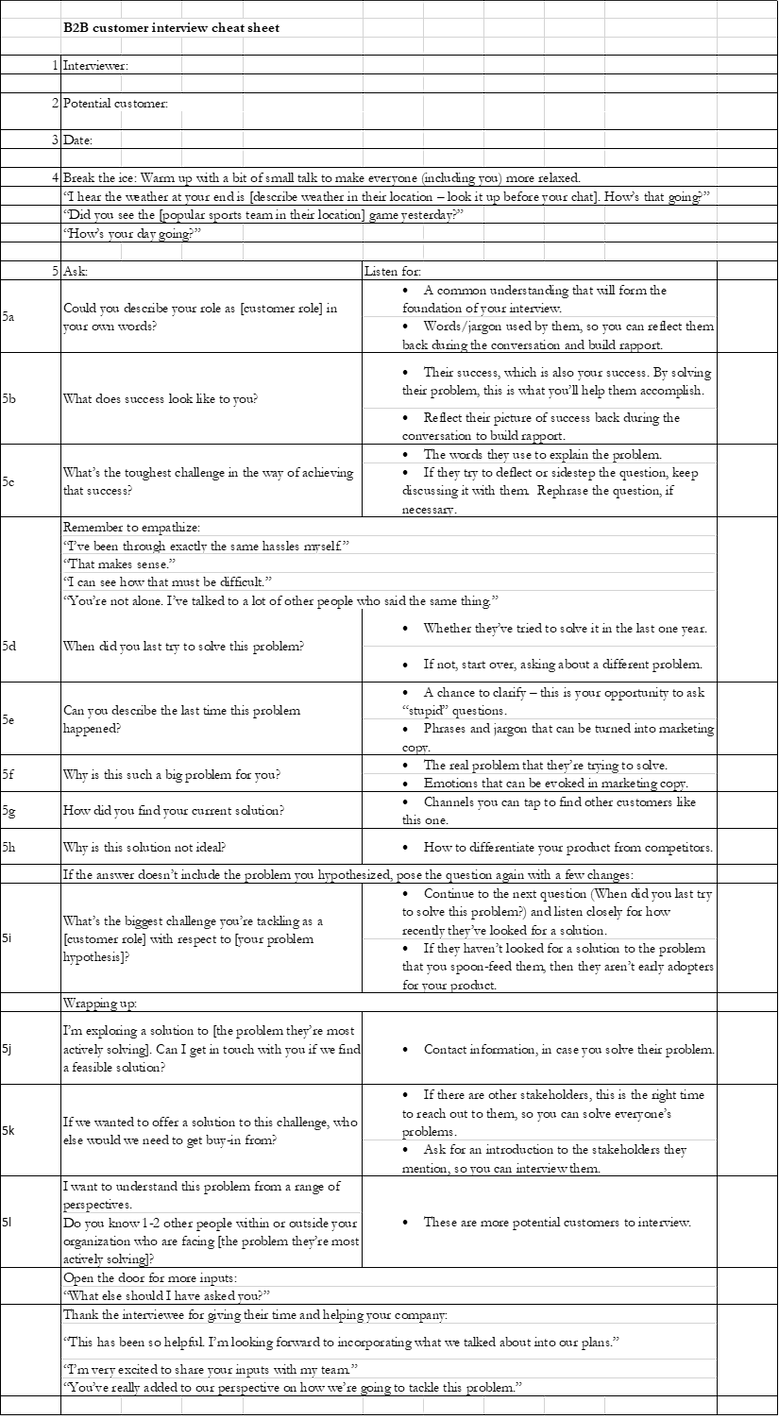

You can validate the problem by interviewing potential customers from your chosen segment. To get the most out of these conversations, you’ll need to prep.

Entrepreneurship expert Steve Blank recommends coming up with at least 100 potential customers to interview. This may sound overwhelming, but it isn’t really that difficult. Remember, you can draw on social networks like LinkedIn and Facebook.

You also have to find the right people to talk to. When it comes to B2B sales, you may want to go straight to the CEO of a company, thinking that you’ve already got everything in perfect shape. That could be a disaster!

Especially in big companies and when you don’t have years of personal experience with the problem you’re trying to solve. In Blank’s words: “You don’t want to start with the highest-ranking person in the company. You want to start in the middle of the company, so you can learn exactly how wrong you are.”

In addition, aim for face-to-face or video conversations – online surveys and emails simply aren’t good enough. You need to watch the person’s face to read their emotions properly. Are they excited by what you’re saying? Are their pupils dilating? Is their breathing getting faster? You want to be able to see these signs.

This is also why you, as the founder, need to conduct customer interviews personally. Plus, if your hypothesis is proved wrong, only you have the authority to decide whether to iterate or pivot. Don’t outsource this critical task to consultants or junior employees.

Remember, these conversations are not for talking about or selling your solution – keep your focus on understanding the potential customer’s challenges.

This might be a little uncomfortable at first. At large companies, they sometimes can’t believe you aren’t pitching a product! So, it’s helpful to explain that you’re not trying to get them to buy anything right now. That you’re there to listen and understand how their business works – and how you can make it better.

Blank advises setting the scene in phone calls and emails before the interview, otherwise “you might end up with 15 people in a boardroom expecting a major presentation”. Giving them a heads-up will help to keep things relaxed and casual.

As for the interview itself, your ultimate goal is to find out the challenges your potential customer is facing – but in a B2B context, that can be an awkward question to start with. In the world of business, people aren’t used to a stranger asking about their company’s problems.

Instead, begin the conversation by focusing on the person’s job: how they define it and what success looks like for them. This helps you understand how their role differs from another individual’s role at a different company. For example, an HR manager’s role at company A might be very different from an HR manager’s role at company B.

You need to grasp how your potential customer sees their role and responsibilities. As they respond, make a note of the keywords and jargon they use. Refer to these over and over during the rest of the conversation. This will also help you to create a mental framework of what their job is like.

Finally, you can maneuver the conversation toward the challenges the person faces in achieving their version of success.

You can use the cheat sheet below as a rough guide for your conversations.

Keep in mind that all the people you contact won’t become interviewees. Some won’t be available, others won’t be available in the period you want, and some will book meetings but postpone at the last minute or fail to show up. So, if you want to set up 5 interviews, contact at least 30 people to reach your goal quickly.

Finally, don’t rely on interviews via introduction. While these are low-hanging fruit and easy to get, it’s very rare that the person you’re being introduced to is actually in your segment. In other words, it’s unlikely that they’re a decision maker for the problem you’ve hypothesized.

Let’s say you want to sell something to P&G, and you have a friend who could introduce you to a friend who works at P&G. What are the chances that the person they’re introducing you to also just happens to be the person with the problem you’re trying to solve? Very, very slim.

An interview with someone who’s not in your segment is worse than no interview at all because it’s likely to lead you down the wrong path.

The second reason not to ask for an introduction is this: a person’s willingness to have a discussion with you about the problem is a very good sign of whether this is a real problem for them or not. If someone is giving you an interview as a favor to someone else, you’ll end up talking to a person who isn’t “paying” to solve the problem – which isn’t a great use of your time.

Basically, although it might be easier to get interviews through introductions, you won’t be able to rely on these conversations to collect data on the weight of the problem or gauge how eager your potential customers are to solve it.

One exception to this rule: if you can get an introduction to a person who’s “paying” to solve the problem, go for it. Just be honest with yourself.

P.S. – While prepping for interviews, you might find it helpful to watch this short video from Steve Blank.

Want to dig deeper and be the best at diving into the customer's mind? Check out the playlist below of 36 videos where Steve Blank goes in-depth on how to nail customer discovery in any and all scenarios.

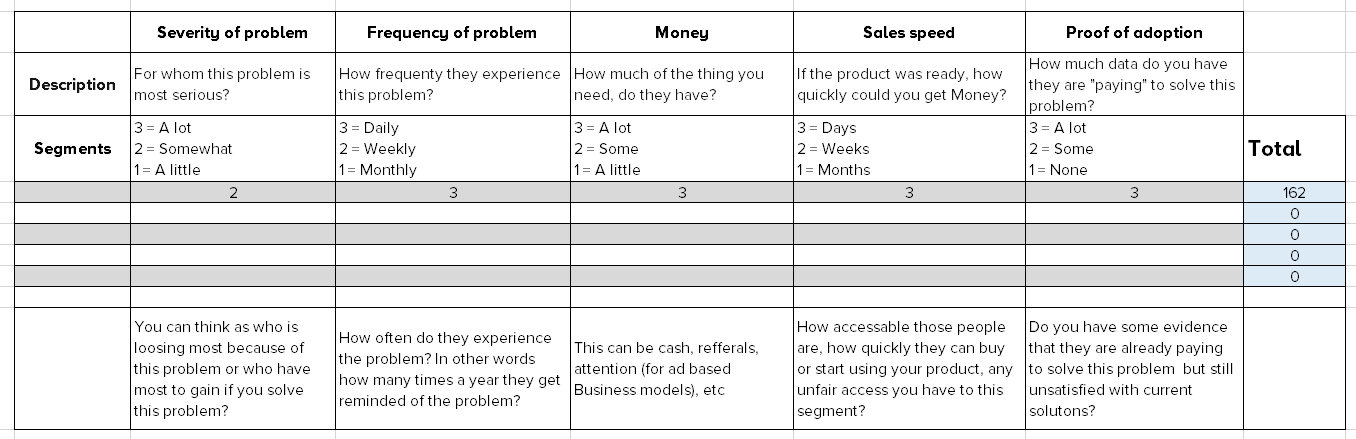

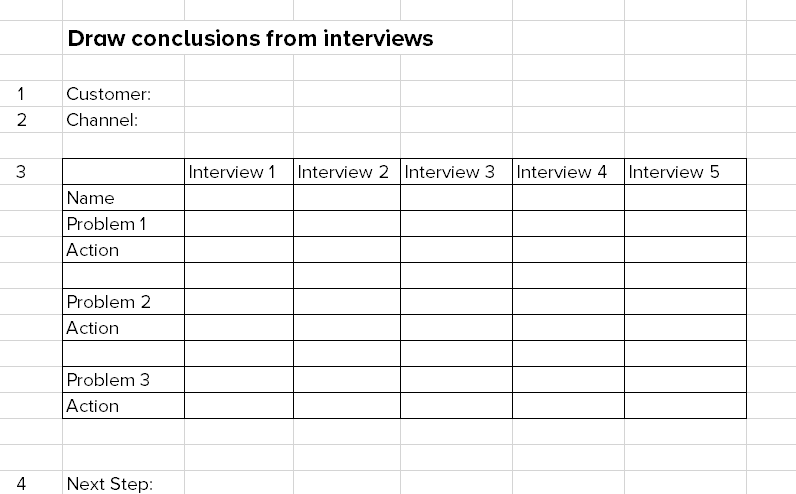

Step 4: Analyze the interviews.

As Steve Blank puts it, “Customer discovery is finding patterns in the data.”

Fill out the above form to analyze your interviews and draw conclusions. Here, “problem” is how your interviewees describe the problem, and “action” is what they’re currently doing to fix it.

If none of the people you interviewed are taking any action, then either the problem isn’t serious enough or they’re not aware that they even have a problem. At the very least, these people won’t be your early adopters.

On the other hand, you know you have a positive pattern if at least 3 out of 5 of your interviewees mention the same type of problem. When you find your early adopter segment, you’ll start to see an eerie similarity in the problems they’re trying to solve.

With a clear problem pattern, you’ll know:

How to define and find your target customers (at least a few of them).

How they think about their problem and what words they use.

Who your major competitor is – and who you need to be better than at solving this problem.

However, if you don’t see a pattern and realize that one or more of your assumptions about those customers were wrong, move on to the second segment from your level 2 segmentation (under Step 2 above) and repeat this exercise. Keep repeating until you see a clear problem pattern among your interviews.

You might also want to keep an eye out for buried hints. Perhaps a couple of your potential customers mentioned a related problem that they’d be willing to pay big bucks to solve – that could definitely be worth exploring.

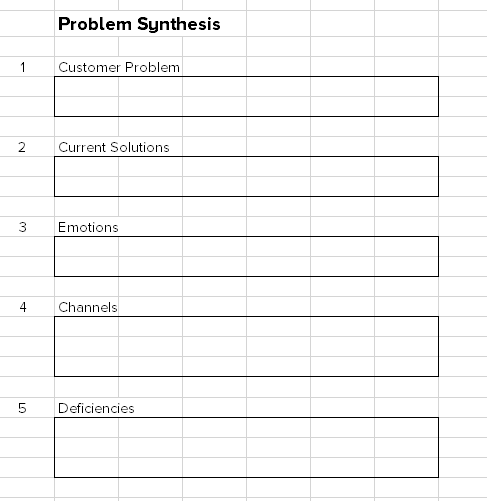

Step 5: Clarify the problem profile.

Ultimately, you should have a problem profile that looks like this.

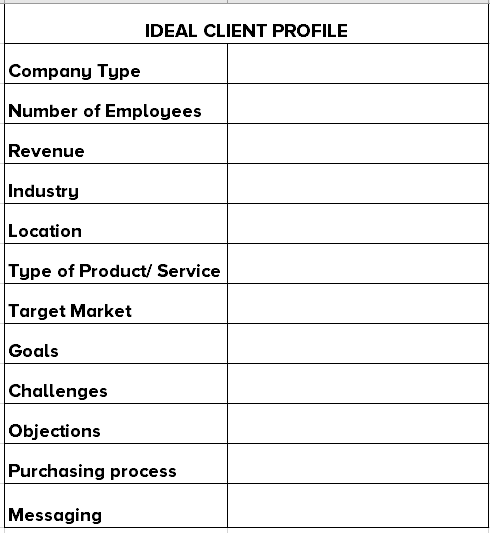

By this point, you should also have an ideal client profile (ICP).

Your ICP maximizes sales and marketing productivity by helping you do two things:

Find great prospects more easily through smart targeting.

Disqualify poor prospects more quickly.

To put it simply, ICP is a template to define your best customer as of right now. This will shape everything else about your company – the product, sales process, channels, and partners. And that, in turn, will drive your success or your failure.

So, it’s critical to define your ICP as accurately as possible, based on your current knowledge.

Keep in mind that ICP isn’t the same as a buyer persona. ICP is a composite description of an organization (company, government agency, or nonprofit) that finds a specific value in your offering and provides excellent value to you in return. Whereas a buyer persona is a profile of the decision-maker in that organization.

Creating your ICP helps you identify the types of accounts that will deliver on the key economics for your company, like close rate, potential revenue, sales velocity, and retention. It also forms the basis for your target account list, priority setting, and qualification criteria.

Remember, this isn’t a one-time exercise. The goal of creating your ICP isn’t to define just one type of customer that you’ll focus on forever. It’s to focus on your ideal customer at a particular time, stage, and situation of your company and your product.

2. Customer Success

The next step is to quantify customer success.

Not only do you want to be unique, but you also want to offer something your target customers “need to have” – as opposed to something that’s “nice to have”.

To do so, you must be clear, measurable, and have a timeline. You want people to see the cost of not doing business with you or not buying your solution. You can’t describe your business in general or vague terms, presenting yourself as just another option.

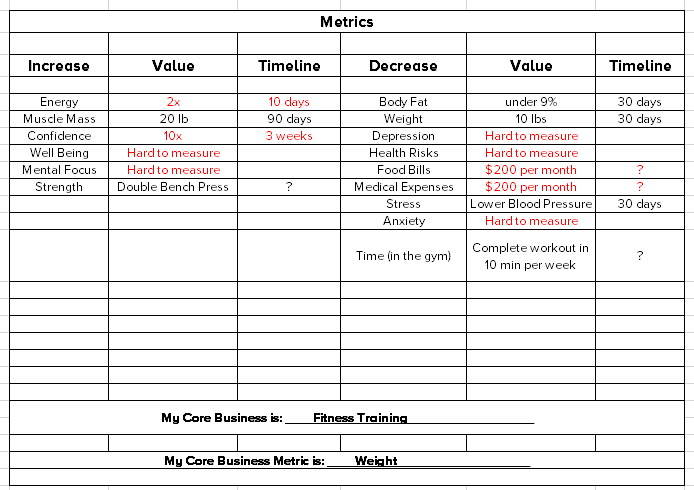

Step 1: Find the metrics.

To begin with, list down all the “metrics” related to the problem space for your target customer. A metric isn’t just limited to money. It includes anything that your solution can help to increase or decrease – time, profit, sales, body weight, energy, and so on.

Then, add a value and timeline to make each metric measurable. This is what gives your solution substance.

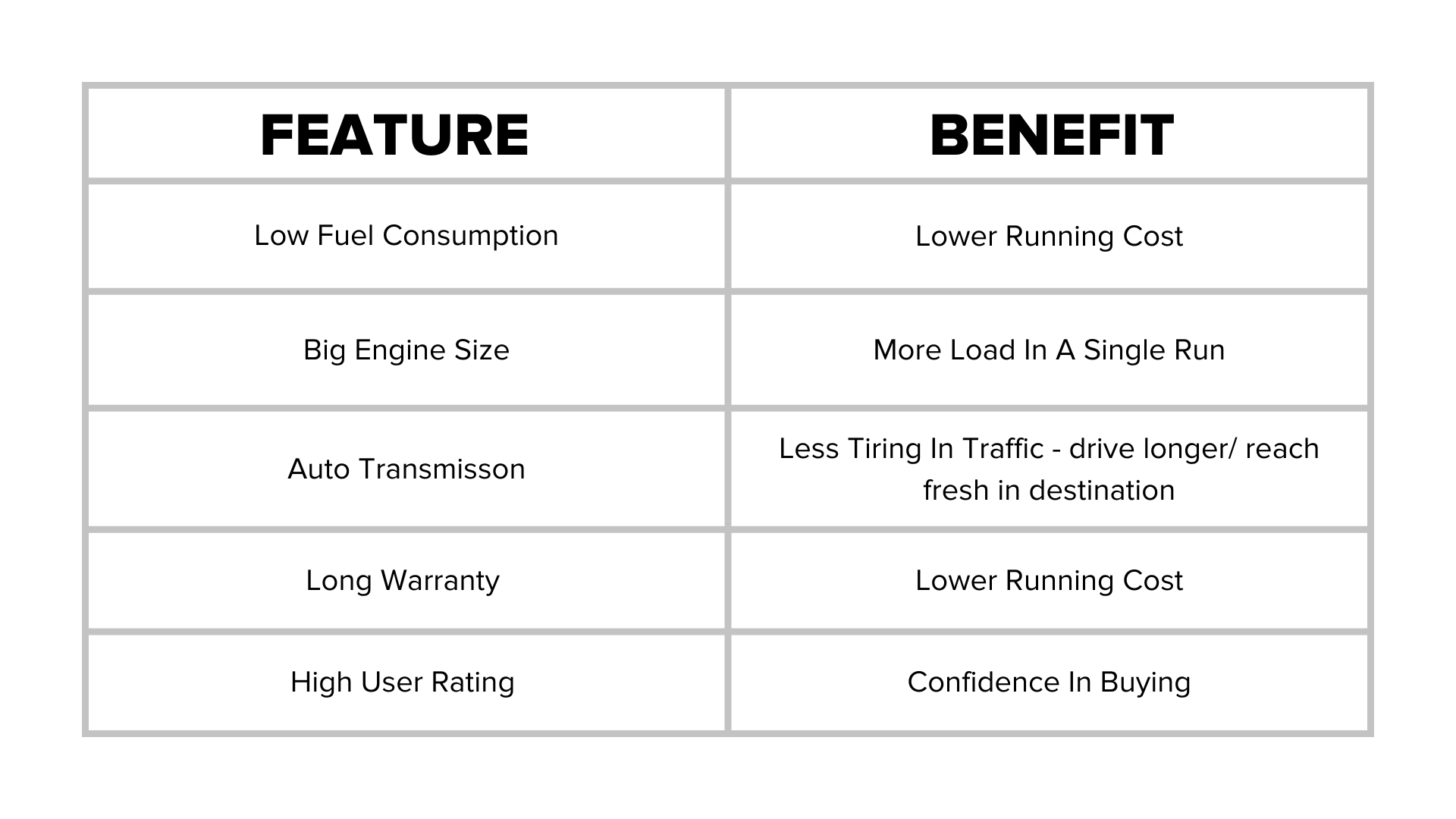

For example, a personal trainer’s metrics might look something like this.

Step 2: Define minimum success.

Now that you know the target customer as well as the specific problem you’re solving, you must define the minimum success you need to deliver in order to make them your customer.

Define what the goal and success look like for your target customer, and pinpoint what steps they’ve taken to achieve success.

For example, the personal trainer might find that the biggest priority for his potential customers is weight loss – not energy, speed, or mental health. For them, success mainly means being thinner.

In such a case, the trainer could decide will simply offer workouts and meal plans that help customers lose a specified amount of weight. This could be good enough to get them to buy and satisfy them. The trainer doesn’t need to do every single thing, like speed training, meditation, stress management, and so on.

Going back to the example of helping independent professionals with taxes: you don’t need to do every single thing for them. Perhaps you found in your interview that independent surgeons end up wasting a lot of time reminding the account departments at hospitals about pending payments. In such a case, sending auto-reminders to hospitals whenever a payment is pending could be enough to make them a customer and satisfy them.

Think of several before-and-after (problem vs. success) scenarios that your target customers might be happy with.

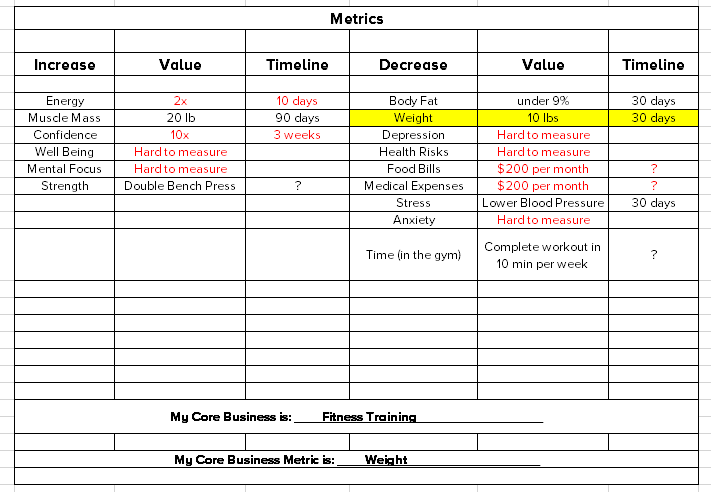

Step 3: Pick a metric.

Based on your metric options and minimum success, you now need to pick one or more metrics for measuring success. When you hit this defined value, both you and the client will definitely agree that success has been achieved.

You’ll see that some metrics are difficult to quantify – like wellness, happiness, peace of mind, and so on. It’s best to leave these out. Choose the metric that’s the most achievable, measurable, and relevant for your potential customers.

For the personal trainer, weight loss is a great core currency. With a metric and timeline, the trainer can make his offering super-specific. He could say, “I’ll help you lose 10 pounds in 30 days.” That’s a measurable success – it’ll appeal to his target customers and motivate them to try out his services. Once he helps them lose 10 pounds, he might upsell them a more advanced program to lose the next 10.

Compare this with a trainer who simply says, “I’ll help you lose weight” without mentioning a specific weight or timeline. Who would you be more likely to buy from?

If you’re struggling to pick one out of multiple metrics, you might not yet be sure about these points:

Which metric does your target customer care about the most?

Which one can you help them achieve the fastest and most easily?

Which outcome can be most effectively quantified?

The best way to figure this out is to create a timeline and solution prototype for each metric. Then examine all your options and choose the one that meets the above three requirements.

IDENTIFY THE VALUE

3. Your Solution

Once you know exactly who your target customer is and what problem you’re solving for them, you can think about solutions.

By this point, you also know (or at least have several hypotheses) the exact measurable metric by which you can prove success to your customer.

This metric is your north star. It’ll be the key to designing possible solutions, prioritizing them, and choosing the best option. It’ll also clear up any confusion you might have about what to include in your minimum viable product (MVP), how you should structure your pricing, or even how to describe your solution to customers.

You’ll use this success metric to show your customer a clear path from point A to point B, from their frustrations to their measurable goals, as no one has ever shown them before. Remember, you need to show them – not just tell them. Once you actually show someone a map with the route and destination, their confidence and trust in you go through the roof.

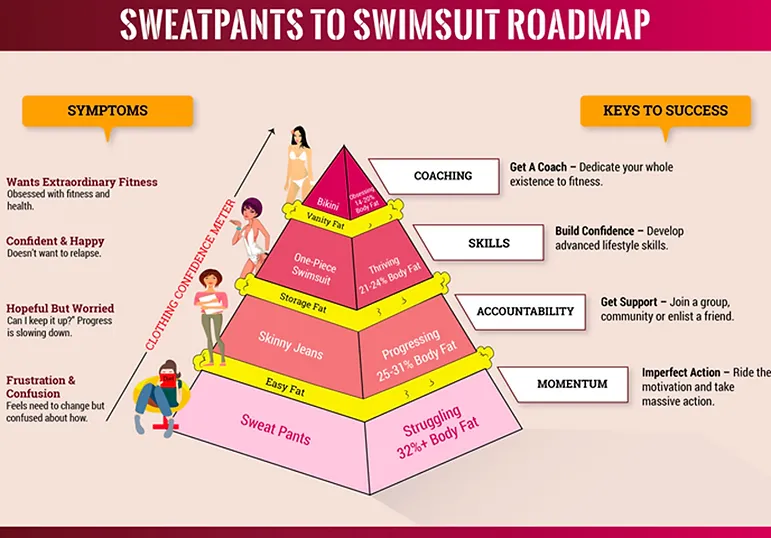

I’ll explain this process using the Sweatpants to Swimsuit Roadmap as an example of a plan a finess trainer might develop.

Step 1

Define their current state. Use the success metrics you selected in the previous step and put a number to their current state. In the above example, you can see this at the bottom of the pyramid – the sweatpants stage, with more than 32 percent body fat.

Step 2

Define the final state. Think about what could be the best-case scenario that’s theoretically possible for your customer to achieve. In the above example, this would be the top of the pyramid – the bikini stage, with 14-20 percent body fat.

Step 3

Create at least three (there can be more) intermediary steps or values of the metrics that can be achieved. These are the three big blocks or milestones of success that you can help your customer to achieve. Think of them as midpoints 1, 2, and 3.

In the above example, there are two intermediary steps between the initial sweatpants level and the final bikini level, i.e. the skinny jeans stage and the one-piece swimsuit stage. Each of these has a metric attached to it (the body fat percentage).

If the steps are quite large, you can further divide each into more steps.

Another way to think about it: imagine you’re writing a book to explain to somebody how they can go from point A to point B. How would you define your chapters?

Step 4

Brainstorm potential solutions from point A to midpoint 1, then to midpoint 2, and so on – all the way to point B. In the above example, you can see the different keys to success on the right.

You don’t need to think of each and every detail of the solution. Just come up with ideas that are plausible and grounded in reality. At the moment, these are simply hypothetical.

Step 5

Create a timeline and identify what your customer needs to do vs. what your product will do for them, based on the solutions you came up with in Step 4.

Define each step (including sign up, grand access to x employee, sync data, upload file, etc.) your customer will need to take from point A to midpoint 1.

In the above example, this would mean describing in detail how you’d get the customer from the sweatpants stage to the skinny jeans stage – e.g. a personalized fitness approach, daily workouts, diet meal plan, motivational app, etc.

Step 6

Create a prototype of your solution that takes the customer from point A to midpoint 1.

While you should have a general idea of the timeline and major steps between point A and point B, it’s really important that you go into detail only between point A and midpoint 1 at this stage.

This is important because:

It helps you to avoid polluting your testing with the customer or their buying decision with details about going from midpoint 1 to point B.

Firstly, the timeline and major steps will probably change when you sell the solution to the first few customers and get a better understanding of how they go from point A to midpoint 1.

Secondly, if your customer never reaches midpoint 1 successfully, nothing else matters anyway. In the above example, if you can’t even get your sweatpants-wearing customer to get into a pair of skinny jeans, then a bikini is out of the question!

At the same time, your ideation of all the points will make you look like somebody with a plan and vision. And it’ll show your customers how much better their lives can be at point B if they just sign up – so that you can prove to them that it’s real by taking them to midpoint 1.

In other words, if you can get someone from sweatpants into skinny jeans, you’ll win their confidence to go with you the rest of the way.

Once you’ve validated your mockup details for taking your customer from point A to midpoint 1, your MVP will simply be the minimum thing you need to do so your customer can reach midpoint 1.

So, you can see how identifying the success metric answers all the questions about what features you need to build.

Later, as you sell to your first customer and while he is in the process of reaching midpoint 1, you’ll simply add things to your product that are the minimum requirements for him to go from midpoint 1 to midpoint 2. That way, your current customer won’t churn and will see a clear path ahead when he reaches midpoint 1.

Offer to test

If you skip offer testing and go straight to selling something, or worse, straight to building something, your experiment will probably fail.

Failure isn’t bad in and of itself – after all, lots of your experiments will fail. What’s worse is that you won’t know why you failed. You’ll have wasted time, money, and energy without knowing how to address the problem or what you need to do differently.

Did you price your solution wrong? Was your marketing copy ineffective? Did customers not trust the product? Was the wrong channel used? With so many variables to test, you’ll probably drain your resources before landing on the winning combination.

To avoid this costly confusion, now that you have multiple metrics and a solution corresponding to each metric, it’s time to go and test with your target customer.

This is where you make prototypes or wireframes and test them with your customers. You can start with the people you already interviewed for the problem.

I highly recommend that you conduct the first round of testing face to face or via video because it’s important for you to see the emotional reaction of the customer – their body language and facial expressions. You don’t want to fall into the trap of polite people saying, “this is interesting”.

Remember, at this stage, selling isn’t your main purpose, so don’t start pitching and demo-ing your “awesome” solution right away.

Instead, focus on verifying if the solution you have in mind is correct from the customer’s perspective of the problem. Are your success metrics and solution a good enough fit to make them buy? Pay attention to these points:

What words do they use to describe your solution?

How do they see your definition of success?

How do they see the things they have to do to achieve success?

How do they see the success metric you came up with?

Using collaborative solution interviews gives you a chance to team up with your customer to create a solution that meets their needs as well as yours. Here’s how to go about it:

Ideally, you should have more than one solution, success metric, etc. as a backup to test in the same meeting, in case your number 1 hypothesis doesn’t resonate with your target customer.

Since you now have a list of metrics, ask about them one by one and see which one gets your customer most excited.

Once you identify that metric, you can present the solution prototype you’ve designed corresponding to that metric.

Don’t show the customer each and every feature and detail you’ve imagined.

Just show them the steps they have to take to achieve success in that metric. Also explain how long it’ll take for them to tangibly achieve, realize and measure success.

Validate your assumptions. Check that the timeline and actions they have to take are not only aligned with their thinking but also more than satisfactory.

Ask them to share their thoughts and feelings as you show them your solution and they ‘progress’ through your solution towards success.

Ask if they think you’re missing something, or if any of your assumptions are not completely right.

You can also use the Three P’s to structure your collaborative solution interviews:

Problem recap. Start your interview by recapping the problems that you understood in your initial interviews (i.e. the problems that brought you together). This is an opportunity to make sure you’re on the same page, as well as remind the potential customer of what you’re both looking for in this exchange.

Proposed solution. Next, share the solution you’ve come up with, based on your initial interviews.

Progression discussion. Finally, ask the potential customer something like, “What do you like and what don’t you like about this solution?” This is your chance to have a dialogue about whether this solution will work for them, and what they think could stop you from progressing.

Along with helping to define your metric ladder, this will also highlight which steps in the ladder they see as most difficult to climb. From there, you can collaborate on ways to make the journey easier for everyone.

Remember, even if you get your metric right, your solution may not be 100 percent perfect.

If that’s the case, don’t worry. Now that you’ve validated the target customer and the metric they care about most – and they can see a possible solution – even if you get a couple of things wrong, they’ll still be interested in helping you get everything right.

They might also introduce you to people in other departments of the company to get a more detailed understanding of how you can refine your solution to deliver success.

On the other hand, if the customer likes both your metric and your solution, that gives you a solid grasp of the minimum you need to build in order to get them to the first step of success. With someone who seems excited and tells you that the solution is a perfect fit for them, you need to pre-sell right away.

Pre-selling lets you test whether you’ll be able to achieve success before investing heavily in actually building a solution. If you’re not able to meet your success goals, there’s no point in building your product.

So, as soon as the customer validates your assumptions about metric and solution, that’s your chance to test if they’re serious about buying. Sometimes, people are engaged and want to help you out but have no real intention of buying. If that’s the case, you need to know as soon as possible.

If they were just being polite, they’ll probably say something like: “Your solution is great, but it’s not really applicable to us.”

Another possibility is that there’s still something missing from your solution, which is holding them back from buying it. Or, maybe the person you’re speaking to isn’t the correct decision maker or needs further approvals. You won’t know any of this unless you try to pre-sell.

Once again, though, you should only pre-sell if you clearly see that the person is excited, and it seems like a really great fit to you.

If your pre-selling attempt goes well, the goal here could be to get a pre-order.

A pre-order is any situation where someone puts money down based on the promise of a product to come. Kickstarter is a good example of this type of “ask”. Pre-orders work for both B2B and B2C.

If you’re unable to produce the promised product, you can offer your customers a refund. Or, you could simply not take their money right away – i.e. not charge their credit cards until the product is completed.

Remember, a pre-order doesn’t really count unless you get the customer’s credit card information or a contract in writing. Even if the contract is conditional on a subjective condition like "if they like your first version of the product".

Although putting down money is the best indicator of intent to buy, you can also test your potential customer’s seriousness in other ways.

For example, you could get a letter of intent. A letter of intent states that if and when you provide a solution that meets their requirements, the company (which is your customer) will pay you the agreed-upon price to buy the product.

This is a non-binding agreement that has no real legal weight. The idea isn’t to force a binding contract. Instead, the goal is to go through the process of getting buy-in from all the right people – they are the ones who will need to sign off on the letter.

Often, this is the same process you’ll need to go through to get your solution approved and adopted by the company. If they’re willing to go through the entire process for a letter of intent, chances are they’ll do the same for your product.

To put it simply, a letter of intent is an excellent way of testing the customer’s commitment before you actually invest in building your product.

So, how can you persuade your potential customers to sign a letter of intent? Here are a few compelling reasons you can offer them:

For the long-term sustainability of your business (which would benefit them as well as you), you want to ensure a minimum number of committed customers before proceeding with the solution. Any business will be able to understand this line of thought.

Letters of intent are valued by investors and will help you raise the investment capital required to build the solution. So, your customers can actually help you fund the company without touching any of their own money.

This works in non-profit contexts as well. Letters of intent can help you get large grants and donations.

You can find lots of example letters of intent online. Choose a format that best suits your company and situation, then tweak it as you like.

Another non-cash method to test your customer’s intent to buy is a detailed collaboration contract for building your product. While they might not want to pay money to build your product, they could be interested enough to provide access to the knowledge and facilities you need.

You could also try to get a signed contract or, if it’s too early for that, a memorandum of understanding (MoU). An MOU is a non-binding contract with no real legal weight. Like a letter of intent, the simple fact of signing it is a sign of seriousness.

The entire point of testing can be summed up as: “If they come, you will build it.”

4. Product Pricing

Let’s first take a look at some fundamental principles of pricing.

The first principle is: Costs do not determine the price.

Price has everything to do with how much your customers are willing to pay. In other words, your costs don’t drive your pricing – your customers do.

Sure, costs play a role. They determine whether it’s feasible to build the product you want. If the price customers are willing to pay is less than the cost of building the product, it obviously isn’t feasible to proceed. But beyond that, costs have little to do with pricing.

The second principle is: Humans can’t infer prices.

We humans find it tough to look at something and determine its value. For example, check out the car in this picture.

Unless you have a ton of background knowledge on cars, you have no way of pinpointing their current value. It could be US$ 2,000, US$ 20,000, US$ 2 million – who knows? Without some additional information, you can’t know for sure.

The additional information we use to figure out a product’s value is the pricing of other products.

The third principle is: Price implies quality.

Before buying, customers assess the quality of a product in different ways. For example, social proof like recommendations from friends, Yelp ratings, testimonials, and so on.

Customers also use other “proxies” to figure out the product’s relative value. For example, its design and aesthetics. If a product looks great on the outside, it’s easy to imagine that it looks and works great on the inside – and the other way around!

That’s why a luxury car seems to have higher quality, even if its actual functionality might be the same as a cheaper car. The same goes for a haircut: getting a trim at a basic chain salon feels different from a high-end salon with all the bells and whistles.

The other proxy customers often use to judge quality is the price.

A higher price doesn’t actually mean better quality – it simply implies it. This perceived increase in quality also boosts sales, up to a point.

Let’s take a look at the relationship between pricing and quality perception.

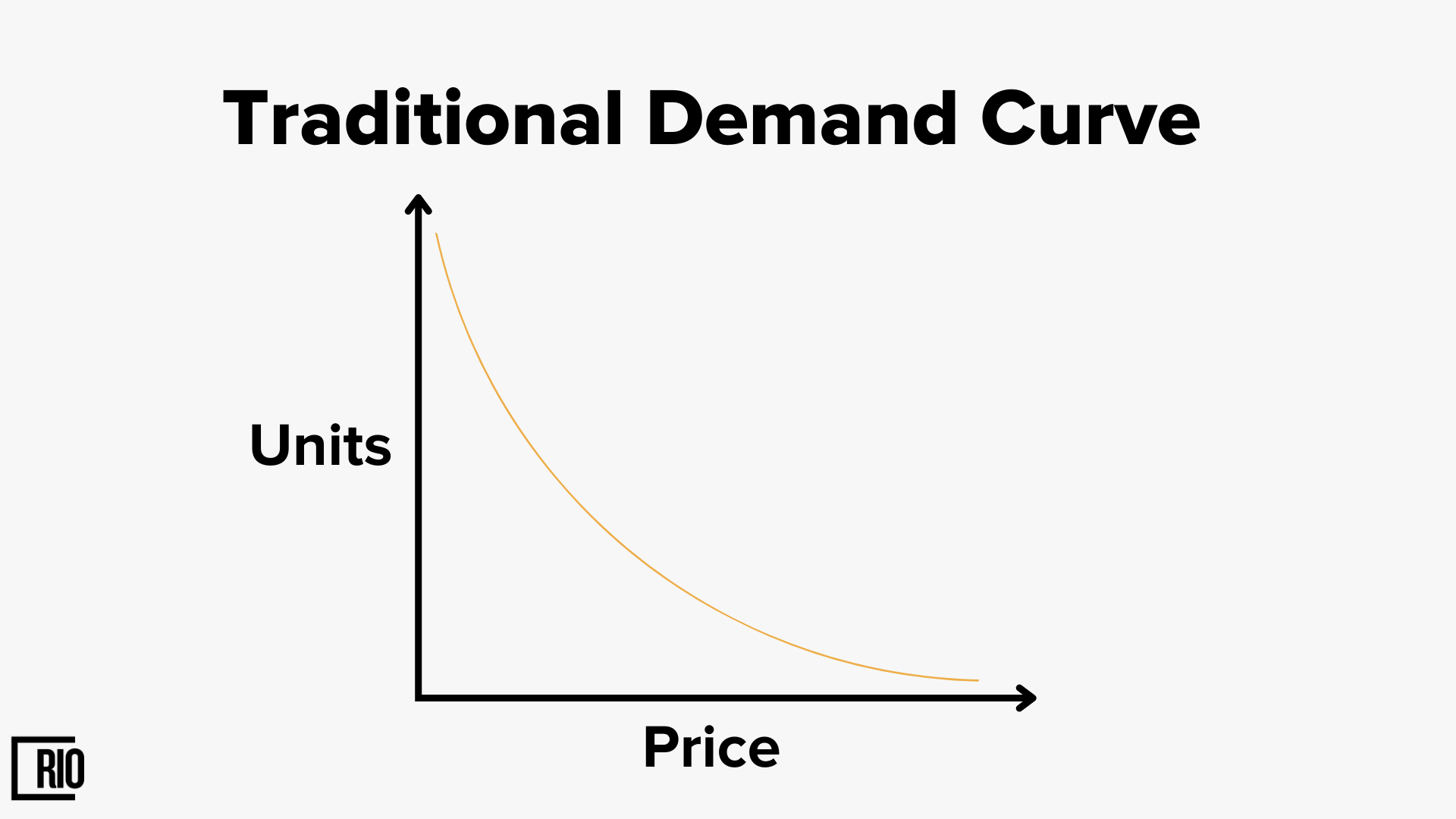

It’s generally thought that demand follows a simple path: as price increases, sales decrease. The logic here is that the cheaper a product is, the more people will buy it. The more expensive it is, the fewer people will buy it.

As it turns out, the idea behind this generally accepted demand curve is wrong when it comes to innovative products.

Professor Ding conducted tests in which the same product was presented at different price points to see what effect price had on sales. Over and over again, he found that price was seen as a sign of quality; up to a point, higher prices increased sales.

Based on these findings, Professor Min Ding concluded that the demand curve looks more like this.

In this curve, you can see that at a very low price, often free, a large number of products are sold. People like free things.

At a slightly higher price, sales drop pretty drastically.

However, at an even higher price point, sales actually begin to increase.

Of course, there’s always a limit. At some point, the price becomes too high and sales start to dip again.

Look at that “bump” in the middle. Your aim should be to identify at what price that bump is highest, so you not only maximize sales but also total revenue.

Unfortunately, many early-stage founders undercharge of their products. The fear of losing customers because of too high a price point is so great that they end up underpricing their products.

By pricing your product too low, you’re making a statement about the quality of your product. You’re saying your solution is of bad quality. And this will ultimately mean you’ll sell less, not more.

Instead of fear, you need to use logic while deciding on the price of your product.

That’s why I’m a huge advocate of value-based pricing. That means you define your pricing based on the value you provide to your customer. What does your product help your customer with? Does it save them time and/or money? Does it help them make more money? Does it reduce risk? Does it make it simpler for them to comply with regulations?

Always try to put a cash amount on the value a customer gets by using your product. Value-based pricing has two main benefits:

You can potentially begin at a higher price point if you can show a higher value-add and justify the price to your customers.

You can raise your prices as you find out more about your customers and add features to your product that provide greater value.

Now that you know what success looks like and how your target customers measure it, you also have a good hypothesis for what your product is worth to them. So, at least in the B2B scenario, you can figure out the answers to these questions with some certainty:

Is your solution making them money? If yes, how much?

Is your solution saving them money? or time? If yes, how much?

Is your solution related to compliance? What is the average cost per year if they don’t comply?

A good rule of thumb is that you can charge at least 10 percent (if not more) of the value your customer is receiving thanks to your product. This is a logical starting point for your pricing. Not only is it justifiable but will also probably be perceived as fair by the customer.

Plus, this further gives you an idea of your average annual revenue per user/customer.

Once you’re clear about your pricing strategy, you can move on to addressing external factors like competition and substitute products.

Start by analyzing the pricing in the market and among your competitors. Invest some time into listing and assessing the packages and pricing offered by your competition.

Don’t forget to check out substitute products that can solve your customer’s problem in a very different way. For example, the biggest competitor for a business class seat in one airline isn’t another airline but a good quality web-conferencing system.

Since people can’t infer prices, they use comparison to analyze whether an item is too expensive or too cheap. This “anchoring” happens in different ways:

What is the cost of not buying a product?

What are the substitute products and the value they provide? Substitute products are your indirect competitors.

What have they paid in the past for similar products?

What are the value and pricing of similar solutions? What about your direct competitor?

What is the original value vs. discounted price? You may have noticed that in supermarkets, some items seem to be permanently on discount. That means they’re trying to anchor a higher price.

Your first priority is to anchor your price in the value your product delivers, i.e. a percentage of time saved, or money saved/made thanks to your solution. What percentage to take, however, is often not clear. While 10 percent is a good rule of thumb, it doesn’t apply in each and every situation.

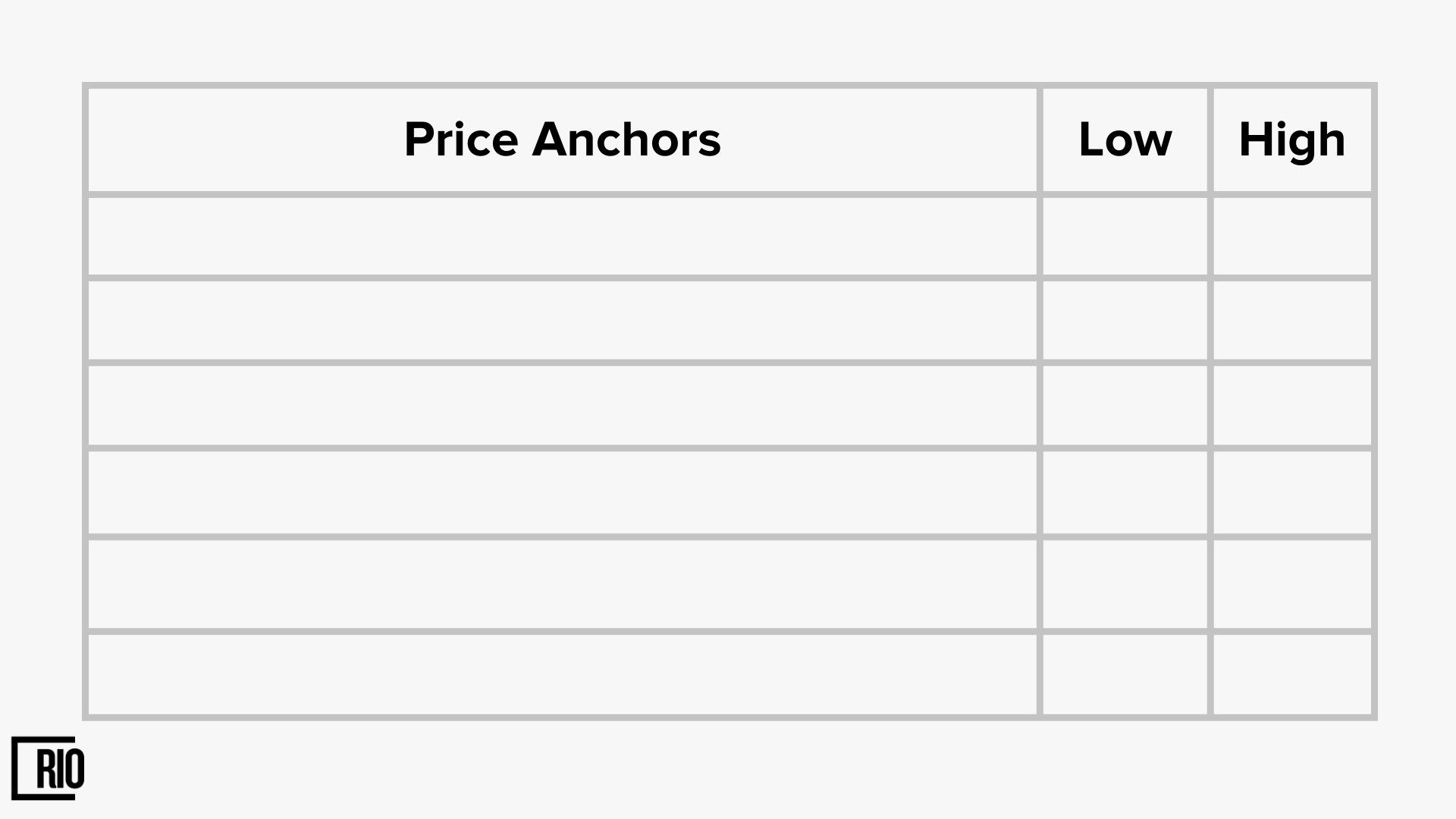

In such a case, anchors from the outside market can help you reach the highest justifiable price.

Use the table below to list all the anchors your customer could take as a reference when thinking about the value vs. pricing of your offer. Mention low-end and high-end pricing for each anchor.

Then, take the anchors that are most comparable with your solution. From among these, take a reference price between the highest-priced anchor and the high value of the lowest-priced anchor. This should give you a good point of reference for determining your own product’s price.

Remember, at this stage of your startup, you don’t want your solution to be seen among the cheapest options – unless being cheaper than everybody else is your UVP.

As you begin with one target segment of customers, start with one pricing plan until you achieve the product-market fit for this segment. In the next round of product-market fit, as you expand to another target segment, you’ll go through the whole process again and create another pricing plan tailored to the new segment.

REACH THE MARKET

5. Customer Outreach

Messaging.

A great customer experience starts with the right messaging. That means focusing on what your customers need – as opposed to what you offer.

It’s important to understand that customers don’t care nearly as much as you do about detailed feature descriptions and what technology you’ve used to build your product. In the beginning, they simply need to know at a high level if you and your product can solve their problem and what benefits you can bring.

In other words, they need to know your Unique Value Proposition (UVP) and Unique Selling Proposition (USP).

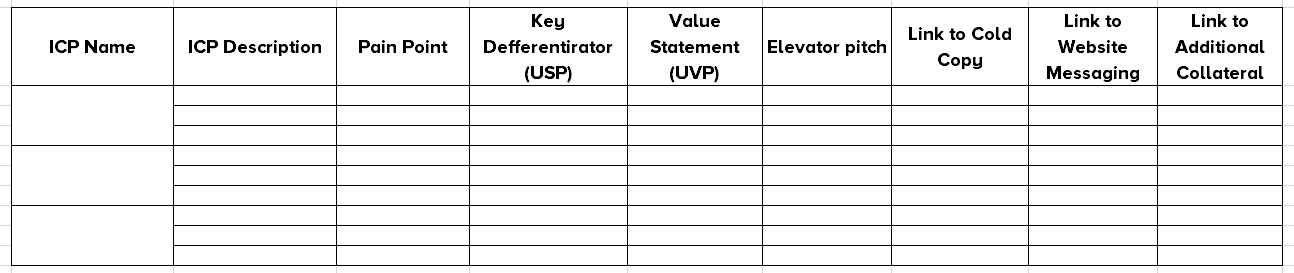

The goal here is to design the first messaging for ideal customers and buyer personas for each channel that you later use in validation. As an early-stage startup founder, what you essentially need is an excellent elevator pitch – this should capture your UVP and USP in the most direct, understandable way for your ICP.

All these terms can get confusing really fast, so I’m going to break them down for you now.

An Elevator pitch is a short statement that defines who you work with (target market) and the general area in which you help them.

About 10 seconds long, the elevator pitch is used mainly at networking events to attract potential clients and start a discussion.

Here are a few elevator pitches in which people describe what they do:

“I work with small companies that are struggling to sell their products or services to big corporate accounts.”

“We help technology companies effectively utilize their customer information to drive repeat sales.”

“I help small-to-medium-sized manufacturing companies that face challenges due to unpredictable revenue streams.”

USP vs. UVP

USP is what a product does, and UVP is what it does for someone. A quarter-inch drill bit drills quarter-inch holes – that’s the USP. It allows me to make my kids happy by hanging a picture on the wall – that’s the UVP.

UVP is a clear statement of the tangible results a customer gets from using your products or services. In other words, it’s what you do for your customer.

A strong UVP is specific, often with numbers or percentages. It could include a snapshot of your work with similar customers as proof of your capabilities.

For example: “We help large businesses to reduce spending on their benefits programs, without affecting the level of services. As healthcare costs continue to skyrocket, this is a major concern for many companies. A recent client, a big manufacturer like you, was struggling to cut costs in this area. With our help, they were able to save US$ 500,000 in just four months. And the employee benefits remained unaffected.”

USP is a statement about what makes you and your company different from other vendors.

Its main aim is to create competitive differentiation. A USP is often used in marketing materials or talking with customers ready to buy.

Your USP could also include:

Specialization. For example: “We specialize in working with financial institutions.”

Guarantee. For example: “We guarantee service within six hours or your money back.”

Methodology. For example: “We use a unique tool called XYZ to analyze your critical needs.”

Helping customers understand your USP is crucial when they’ve already decided to make a purchase. But it has zero impact when customers are satisfied with their situation or when they’re frustrated but haven’t yet decided to change.

In the world of tech solutions, you can think of USP as the features and UVP as the benefits of those features.

At this point, you know what problem you’re solving, for whom, and how your solution is unique compared to what they were using previously. So, defining your USP should be quite straightforward.

You also know how your customer defines success, what metric he uses to measure that success and how it compares to the current situation – that’s going to be your UVP.

For now, try to keep your USP and UVP short and sweet, using the words of your customers. It’s best to have one-liners – two at most. From these and the ICP, you can derive your elevator pitch.

You can use the table below to develop your initial market messaging map.

Channel

Channel is simply a means to get the attention of your target customers and create enough interest for you to get them on the phone.

For B2B startups, at this point in time, you want a channel that:

Is precise. Your message needs to specifically reach the right decision-makers in your ICP.

Is simple. Your initial message must go via a channel that doesn’t require a long, complicated format or graphics.

Is cheap. The cost per contact should essentially be free. You could need to test and iterate your message several times, and you might also need multiple touchpoints per contact to get things moving.

Has a direct call to action. At this stage, you’re validating your assumptions, testing your message, and selling – all at the same time. So, the channel should lead directly to a phone call or a meeting.

Helps you test and iterate your message quickly to achieve message-market fit.

Out of all the channels out there, the only ones that meet these requirements and are historically proven to work well for B2B are emails and phone calls.

Emails and phone calls are precise and targeted to a particular person. Both are virtually free and can include a direct call to action. For each of them, your short and sweet elevator pitch is basically your message. In your first email or phone call, you can present your elevator pitch, followed by a call to action, e.g. “If that sounds interesting to you, we’d like to book a 30-minute call to explore this further.”

Finally, both channels allow you to contact 20-50 people per week, note how people respond, get feedback, see what works and what doesn’t – and quickly improve your messaging for the next week’s contacts.

For B2C startups, I highly recommend the Bullseye Framework, which will help you identify the right channel to get traction. This involves a five-step process: brainstorm, rank, prioritize, test and focus on what works.

You can begin by tweaking your elevator pitch for different channels, as you use the framework to pinpoint the one that works best at this stage of your company and product. To get an in-depth understanding of the Bullseye Framework, check out Traction: How Any Startup Can Achieve Explosive Customer Growth.

Of course, for both B2B and B2C, as your company grows you’ll experiment with other kinds of channels – outbound as well as inbound – and generate sales without ever having a phone call with customers. You’ll change or add more channels to your market outreach mix to make it more efficient and effective.

6. Calculating Sales

Steps of the sales funnel

By this point, you know exactly what you’re selling, to whom, why they’d buy your product, at what price, and with what message. It’s now time to start reaching out to tens or even hundreds of potential customers while, at the same time, building your minimum viable product (MVP).

You may be thinking: “My MVP isn’t even finished. Isn’t it too early to reach out to my customers?”

The answer is: not at all. In fact, this is exactly the right time, since you want to achieve product-market fit as soon as possible.

You see, making a sale is like getting married – people don’t usually say “yes” and commit the very first time they meet you! It takes time and several meetings. If you reach out today, then you’ll have customers lined up and ready to buy by the time you have your MVP ready.

Along the way, you’ll also have to get feedback on your proposals, get approval at various levels, and see whether your product is being designed and implemented in such a way that the customer can use it to achieve success faster, more easily, or more cheaply. All of this needs to happen before you finally get to the stage where the budget is approved, and you receive your cash.

In addition, some of your potential customers may drop off the face of the earth. The companies you initially contacted might change their priorities. Your contact could switch jobs. Funding sources may change.

You really don’t want to be in a situation where you’re counting on a very small number of companies (say, 1-4) that showed interest in or pre-signed up for your solution – because when it comes down to it, they may not be ready to buy anymore. Then you’d have to start the whole process all over again, from scratch.

So, to maximize your chances of early success, reach out to as many potential customers as early as possible at this stage. This is something you have control over – unlike the possibility of certain potential customers vanishing from the scene.

You probably want to start by using simple channels, like emails, to contact your target customers. Soon, you’ll notice a cycle that’s typical with B2B interactions:

Schedule a meeting, attend a meeting.

Get introduced to the person representing the next step.

Schedule another meeting, attend another meeting.

Get introduced to the next person representing the next step, and so on….

At each step, either your target customer will ask for something or you will (for example, the next meeting, more details, contact with other decision-makers in the company, etc.). Note down and document everything for each prospective customer you contact.

As you have more calls with potential customers ready to buy, you’ll start to realize how many steps and how much time it takes for your customer to actually sign up and buy your product.

This will also shape your sales funnel.

The key here is to document the interaction with each potential customer – this will later help you to identify a pattern. As you interact with several companies, you’ll notice things like:

How much do you have to educate the customer about the problem itself?

Whether you have to deal with one or more decision-makers.

How to help your first contact decision maker to sell the solution internally.

Who else might say no to your solution (for example, IT guys), and how you can help them get on board?

This knowledge will help you define the steps of your sales funnel.

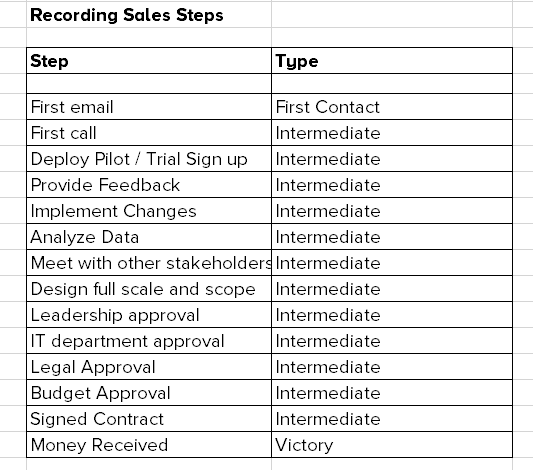

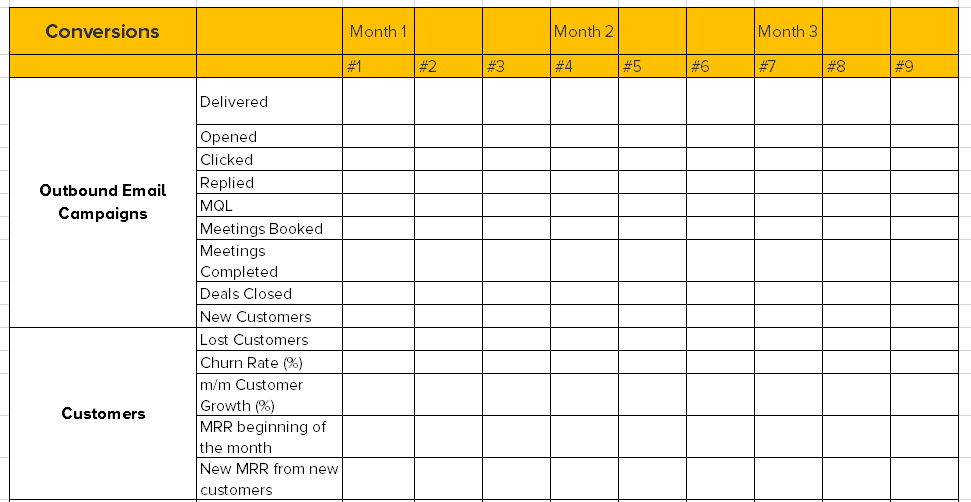

You need to continually reach out to new target customers – say, in batches of 10-20 per week. Keep recording all your data in a table like the one I’ve provided below. As you get 10, then 20, then 30 customers to buy your solution, you’ll get a good grasp of your sales funnel and the steps needed for you to make a sale in the target market.

There are several good CRMs that can help you keep track of your outreach to potential customers. At the most basic level, you can use the template below to keep track of your outreach.

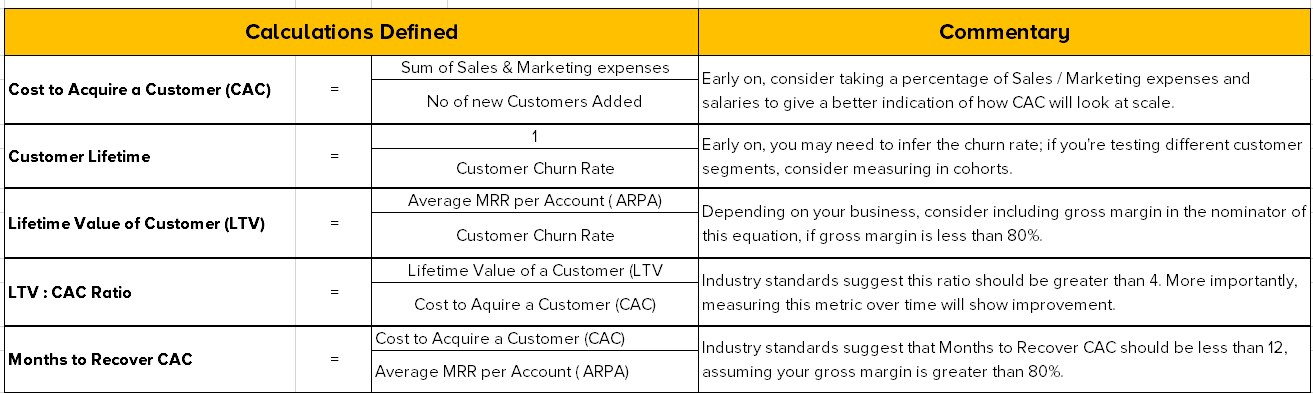

Cost of Acquiring Customer (CAC)

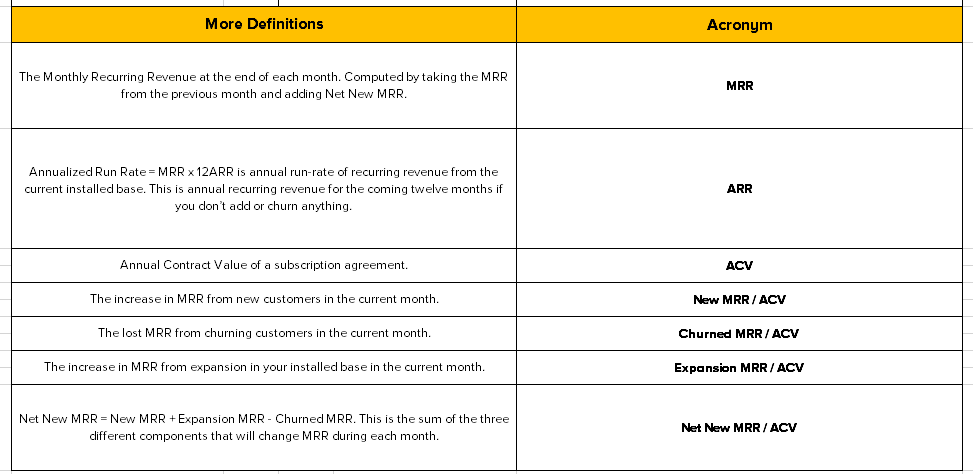

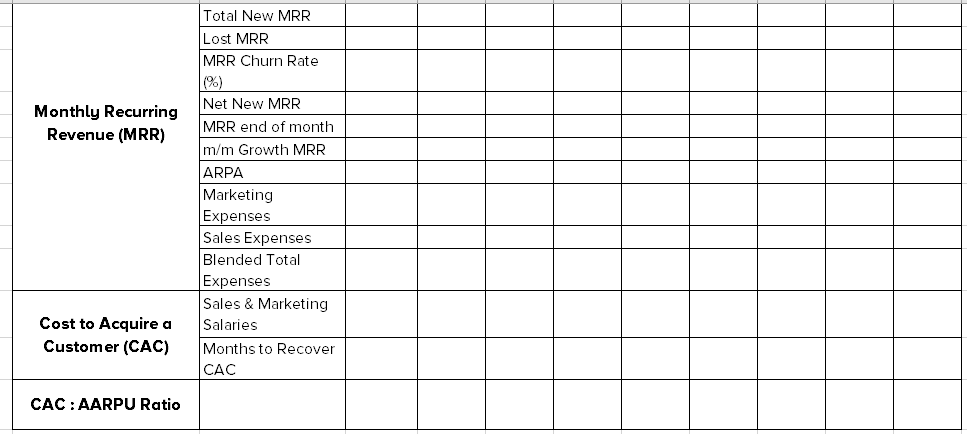

Once you have your sales funnel, getting your CAC and the average sales cycle is just a matter of putting your sales funnel and associated costs in an Excel file.

You have the necessary variables in place already, and I’ve provided the formulas in the table below.

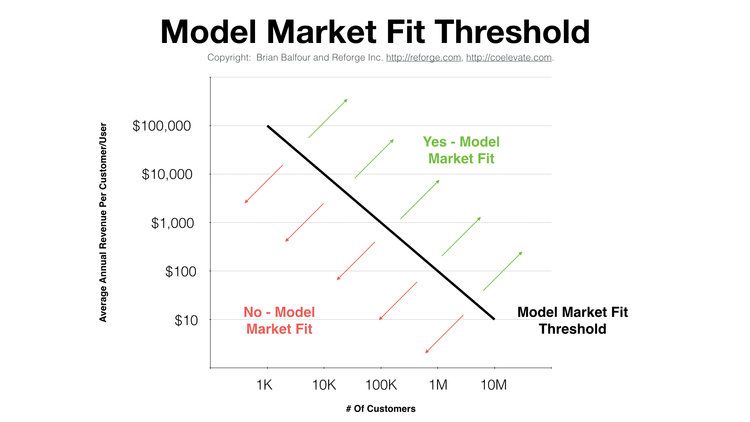

Finally, take a look at Brian Balfour’s Model Market Fit Threshold below with respect to the assuptions about total addressable market of your current ICP. Where do you stand?

If you’re above the line, in the green zone, you’re good. Congratulations – you’ve achieved model-market fit!

However, if your product seems to be in the red zone, you don’t yet have a model-market fit. In that case, go through these points:

Check each step of the process and see if there’s something you can improve, optimize, automate, or get rid of in order to reduce your CAC.

Re-assess your pricing strategy and ask yourself, “Can I charge more?”

If neither of the above is possible for the moment, with the given target customer and solution, then maybe it isn’t possible for you to go green at this iteration of product-market fit.

That might just be okay for now, if you have enough cash to burn while you wait for the next iteration of product-market fit as you expand your customer base, add more success factors to your product to increase pricing, or bring better optimization/automation to your product and lead generation.

Still, in order to be a profitable company, you should start strategizing now to prioritize the options you might have for the next iteration of product-market fit.

x contacts -> y sales -> in z days

The hard work is all done. For this final step, you already have the numbers you need and can easily calculate:

x – how many customers have you contacted?

y – how many sales have you made?

z – how many days it took from first contact/email on average for a customer to buy?

Conclusion

Using the Guaranteed P-M Fit Method, you should now have all the variables you need. It’s time to put them into the product-market fit statement that we defined at the beginning of this article:

Product-market fit is knowing that if today you reach out to [x number] of [target customers] with [a message], you’ll have [y sales] in [z days] with [a, b, and c steps] in your sales funnel, for [a solution] that helps them achieve [success] by solving [a problem] they have while having your [AARPU] more than [CAC].

You have not only achieved product-market fit but also proven it.

On one hand, this makes it possible for you to scale. You’ve reached a product-market fit for your niche, which means your startup is now ready to grow. You’re no longer “figuring things out” – you know exactly how to reach your target segment and how long it takes to make sales.

At the same time, you can start moving forward and thinking about other target segments. For the next niche you choose, you can once again use the Guaranteed P-M Fit Method to achieve product-market fit. In other words, you’re all set to begin expanding as a company.

Which part of this process is most challenging for you?

What’s stopping you to reach product-market fit and be a growth-ready startup?

Download worksheets

This content is for subscribers only

Sign up now to read the content and get access to the full library of content for subscribers only.